Benefits in Kind (BIK): Definition, Table, Calculation Formula

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowBenefits in Kind (BIK) are non-cash perks offered by employers to employees, such as company cars, housing, or medical coverage.

While these benefits help improve employee satisfaction, they also have tax consequences.

Read the article below to learn more about Benefits in Kind (BIK) and how they are valued, reported, and taxed based on the latest BIK table from LHDN.

What are Benefits in Kind (BIK)?

Benefits in Kind (BIK) are non-cash benefits given by employers to employees as part of their compensation package.

Unlike direct salary payments, BIK cannot be converted into cash, sold, or exchanged, even though they have a monetary value.

These benefits range from company-provided vehicles and accommodation to club memberships and free medical care.

BIK is a way to attract and retain talent by providing additional perks that enhance the employee’s work-life balance.

Benefits such as housing, transportation, and medical coverage can make a company more competitive when hiring new employees.

However, BIK also impacts payroll and taxation in Malaysia.

Employers need to calculate and report these benefits correctly because they can be subject to Monthly Tax Deductions (MTD) or PCB (Potongan Cukai Bulanan).

Misreporting BIK can lead to tax complications for both the company and the employees.

What is Considered as Benefits in Kind (BIK)?

BIK is defined under the Income Tax Act 1967 as benefits given to employees that are not in the form of money.

These benefits are different from perquisites, which are monetary benefits such as cash allowances, bonuses, or reimbursements.

BIK vs. Perquisites: What’s the Difference?

To understand the distinction between BIK and perquisites, refer to the following comparison:

|

Aspect |

Benefits in Kind (BIK) |

Perquisites |

|---|---|---|

|

Definition |

Non-cash benefits provided by the employer |

Cash benefits given to employees |

|

Convertibility |

Cannot be exchanged for cash |

Can be received as money |

|

Examples |

Company car, accommodation, utilities |

Bonuses, phone bill reimbursements, allowances |

|

Taxation |

Taxable, calculated using the prescribed value or formula method |

Fully-taxable as part of salary |

The main difference is that BIK involves physical assets or services that an employee benefits from, while perquisites involve additional cash payments.

How BIK is Treated Under Malaysia’s Tax System

BIK is considered part of an employee’s taxable income unless it qualifies for tax exemptions.

The Lembaga Hasil Dalam Negeri (LHDN) provides two ways to determine the value of BIK:

-

Formula method which is based on the actual cost of the benefit and its lifespan.

-

Prescribed value method. This is using predefined values provided in the BIK table.

Types of Benefits in Kind (BIK) in Malaysia

Various forms of BIK are commonly found in Malaysia, which are:

1. Company Cars and Fuel Allowance

Company cars are given to employees in managerial positions or roles that require frequent travel.

The cost of the vehicle and fuel is taxable if used for personal purposes.

The tax calculation depends on whether the company uses the formula method or the prescribed value method.

2. Accommodation and Housing Benefits

Some companies provide free or subsidized accommodation, either in the form of rented properties or company-owned housing.

This also includes utility bills such as electricity, water, and phone bills, which may be covered by the employer.

3. Personal Drivers or Domestic Helpers

High-level executives may receive a personal driver or household staff, such as maids or gardeners, as part of their employment package.

4. Club Memberships and Recreational Facilities

Some companies provide gym memberships or access to recreational clubs to promote employee wellness and networking.

These benefits can be taxable unless they are directly related to business purposes.

5. Employer-Sponsored Insurance Premiums

Employers sometimes cover medical, life, or accident insurance for employees. Some insurance benefits are tax-exempt, especially if they cover workplace injuries.

6. Gifts, Vouchers, and Incentives

Physical gifts such as electronics, travel tickets, or vouchers provided as rewards to employees may fall under taxable BIK.

7. Educational Assistance and Training

Companies that sponsor employees' further education or training programs may need to report these as taxable benefits if they are unrelated to the employee’s job.

How to Calculate Taxable Benefits in Kind (BIK)?

There are two methods to calculate the taxable value of Benefits in Kind:

1. The Formula Method

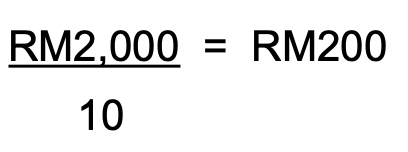

The Formula Method calculates BIK based on the actual cost incurred by the employer and the lifespan of the asset provided to the employee. The formula is:

For example, a company provides an air conditioner for an employee’s use.

The air conditioner costs RM2,000, and according to LHDN’s prescribed asset lifespan table, air conditioners have a lifespan of 10 years.

In this case, the employee's taxable BIK for the air conditioner would be RM200 per year.

2. The Prescribed Value Method

The Prescribed Value Method simplifies BIK calculation by assigning a fixed taxable value based on predefined categories set by LHDN.

These values are outlined in the BIK Table and provide a standard approach without requiring asset lifespan calculations.

For example, an employee gets a company car that originally cost RM100,000.

According to LHDN’s BIK Table, the prescribed annual benefit value for a car in this price range is RM5,000.

Additionally, if the employer provides a fuel allowance, the prescribed taxable value for petrol is RM1,500.

Total Taxable BIK = RM5,000 (Car) + RM1,500 (Fuel Allowance) = RM6,500 annually

BIK Table: Prescribed Value Method (2025 Update)

Prescribed Average Lifespan of Assets for Benefits in Kind (BIK)

|

Asset |

Prescribed Average Lifespan (Years) |

|---|---|

|

Motorcar |

8 |

|

Curtains and Carpets |

5 |

|

Furniture, Sewing Machine |

15 |

|

Air Conditioner |

8 |

|

Refrigerator |

10 |

|

Kitchen Equipment (e.g., Crockery, Rice Cooker, Electric Kettle, Toaster, Coffee Maker, Gas Cooker, Oven) |

6 |

|

Piano |

20 |

|

Organ |

10 |

|

TV, Video Recorder, CD/DVD Player, Stereo Set |

7 |

|

Swimming Pool (Detachable), Sauna |

15 |

|

Miscellaneous |

5 |

Prescribed Value of Benefits in Kind (BIK) Commonly Provided by Employers to Employees

1. The Prescribed Value of Motorcar and Its Related Benefits

|

Cost of Motorcar (New) (RM) |

Annual Prescribed Benefit of Motorcar (RM) |

Annual Prescribed Benefit of Petrol (RM) |

|---|---|---|

|

Up to 50,000 |

1,200 |

600 |

|

50,001 - 75,000 |

2,400 |

900 |

|

75,001 - 100,000 |

3,600 |

1,200 |

|

100,001 - 150,000 |

5,000 |

1,500 |

|

150,001 - 200,000 |

7,000 |

1,800 |

|

200,001 - 250,000 |

9,000 |

2,100 |

|

250,001 - 350,000 |

15,000 |

2,400 |

|

350,001 - 500,000 |

21,250 |

2,700 |

|

500,001 and above |

25,000 |

3,000 |

2. Prescribed Value of Household Furnishings, Apparatus, and Appliances

|

Category |

Type of Benefit |

Annual Prescribed Value of BIK Provided (RM) |

|---|---|---|

|

1 |

Semi-furnished with furniture in the lounge, dining room, or bedroom |

840 |

|

2 |

Semi-furnished with furniture as in Category 1 plus one or two of the following: air-conditioners, curtains, carpets |

1,680 |

|

3 |

Fully furnished, including benefits from Categories 1 and 2, plus kitchen equipment, crockery, utensils, and appliances |

3,360 |

|

4 |

Service charges and utility bills (water, electricity) paid by employer |

Actual cost paid by employer |

3. Prescribed Value of Other Benefits

|

Item |

Type of Benefit |

Value of BIK Per Year (RM) |

|

|---|---|---|---|

|

1 |

Telephone (including mobile phone) |

i) Hardware – fully exempt for one unit per asset category ii) Bills – fully exempt for one unit per asset category |

|

|

2 |

Recreational club |

Individual membership – subscription paid or reimbursed by employer |

i) Entrance fee for club membership – taxable under paragraph 13(1)(a) of the ITA ii) Monthly/annual membership subscription fees – taxable under paragraph 13(1)(a) of the ITA iii) Term membership – taxed under paragraph 13(1)(a) of the ITA |

|

Corporate membership – subscription paid by employer |

(i) Entrance fee – not taxable (ii) Monthly/annual membership subscription fees – taxed under paragraph 13(1)(b) of the ITA |

||

|

3 |

Gardener |

3,600 per gardener |

|

|

4 |

Household servant |

4,800 per servant |

|

Which Benefits-in-kind Are Tax Exempt?

Some BIK are not taxable, meaning they do not increase an employee’s taxable income. These include:

-

Medical and dental benefits

-

Childcare benefits

-

Free meals at the workplace (excluding alcohol)

-

Transportation between home and workplace is provided by the employer

-

Insurance for foreign workers

-

Group accident insurance

-

Discounted goods and services

Are Benefits-in-Kind Tax-Free?

Not all Benefits-in-Kind (BIK) are tax-free. In Malaysia, most non-cash benefits given by employers are considered part of an employee’s taxable income.

This means they need to be reported and may be subject to tax.

LHDN requires employers to calculate and declare taxable BIK using either the Formula Method or the Prescribed Value Method.

However, some benefits are exempt from tax, meaning they do not count as part of an employee’s taxable income.

How BIK Affects Employees’ Taxable Income

BIK directly impacts the taxable income of employees, which means employers must handle tax declarations accurately.

Employees need to declare BIK in their personal tax filings and employers must report them in payroll calculations.

To make compensation packages more attractive, companies can strategically optimize salary structures by balancing cash salary and BIK to reduce tax burdens.

Hire the Best by Offering the Right Benefits

Giving Benefit in Kind (BIK) shows your employees you truly care. Simple things like meal allowances, health benefits, or a company car can make them feel appreciated and happy at work. When employees feel valued, they stay longer and do their best.

Want a loyal and motivated team? Post your job today and hire the right people with the best benefits!

Read More:

- Total Tax Exempt Allowances, Perquisites, Gifts & Benefits in Malaysia (2025)

- CP22 Form: Deadline, Free Download, & How to Fill

- CP204: Deadline, Calculation, & Free Download Form

- How to Use ByrHASiL for Online Tax Payments in Malaysia

- PCB Deduction in Malaysia: Calculation, Rates & Employer Guide

- What is the 182 Days Rule in Malaysia? Tax Residency Explained

- Labour Law Malaysia Salary Payment For Employers

- Best Answers for 'Why Should We Hire You' – A Guide for Employers

- 12 Employment Types You Need to Know: A Guide for Employers

- What is Precarious Employment? Risks, Challenges, and Solution

- New EPF Retirement Savings: Helping Employers Support Financial Well-Being for Employees

- Higher Pensioners in 2024, Government Set to Finalize Pension Rates

- Lack of Diversity in Candidate Pool: Why It Matters and How to Improve It

- Overtime Pay in Malaysia: Legal Requirement and Calculation