Cara Buka Akaun KWSP Anak Malaysia & i-Saraan Benefits

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowMany parents in Malaysia usually keep duit raya or savings for their children in a normal bank account.

This is safe, but there is one problem, the money grows very slowly because bank interest is quite low.

Because of this, more parents are now looking at KWSP (EPF) as a better way to grow savings over time.

What many people don’t realise is, you can now open a KWSP account for your child as early as 14 years old, without waiting for them to start working.

At the same time, this idea is also useful for working adults. It shows a simple lesson, the earlier you start saving, the better the result in the future.

What is a KWSP Account for Children in Malaysia?

A KWSP account for children is a savings account under KWSP that allows individuals aged 14 and above to start saving early.

In simple terms, it works like a long-term savings account, but with extra benefits.

With a KWSP account, your child can:

-

Earn annual KWSP dividend

-

Receive government incentive (through i-Saraan)

-

Grow savings over time through compounding

This helps parents build a strong financial base for their children before they even start working.

What is i-Saraan?

i-Saraan is a voluntary contribution scheme for people who do not have fixed income.

It is not only for children, but also suitable for:

-

Parents saving on behalf of their child

-

Freelancers or gig workers

-

Working adults who want to increase their savings

The main benefits are:

-

You earn KWSP yearly dividend

-

You get extra money from the government (incentive)

Because of this, saving through i-Saraan can be more rewarding compared to normal savings.

KWSP Account Structure

KWSP divides your savings into 3 parts:

-

Account 1 (75%) – mainly for retirement

-

Account 2 (15%) – can be used for education or certain needs

-

Account 3 (10%) – can be withdrawn anytime

This structure is important because it gives a balance between:

-

Long-term savings

-

Some level of flexibility

For example, Account 3 can help during emergency situations without affecting the full savings.

Why Use i-Saraan for Children’s Savings?

If you compare KWSP with a normal bank account, the difference is quite clear.

Government Incentive

When you contribute:

-

You get extra 20% from the government

-

Up to RM500 per year

Stable Dividend

KWSP usually gives around:

-

5% to 6% return per year (estimated)

This is generally higher than normal savings accounts.

Compounding Effect

This is the most important part.

When you start early:

-

Your money earns returns

-

Then those returns also earn more returns

Over time, this can grow into a much bigger amount.

That’s why many parents use KWSP to manage duit raya or long-term savings for their children.

Incentive Limit You Should Know

Even though the incentive is attractive, there is a limit:

-

Maximum RM500 per year

-

Maximum RM5,000 for lifetime

This means you can usually enjoy the full benefit for about 10 years.

Example: 10-Year Savings Growth

Let’s look at a simple example to understand better.

Assumption:

-

Save RM3,000 per year

-

Get RM500 incentive

-

Dividend 6%

After 10 years:

-

Total saved: RM35,000

-

Estimated value: RM46,000

This shows how your savings can grow faster with dividend and compounding.

How to Open a KWSP Account for Your Child

There are 3 simple ways to do it:

1. Using i-Akaun App (Recommended)

-

Download KWSP i-Akaun

-

Select “Register”

-

Complete e-KYC verification

-

Follow the steps

This is the easiest and fastest method.

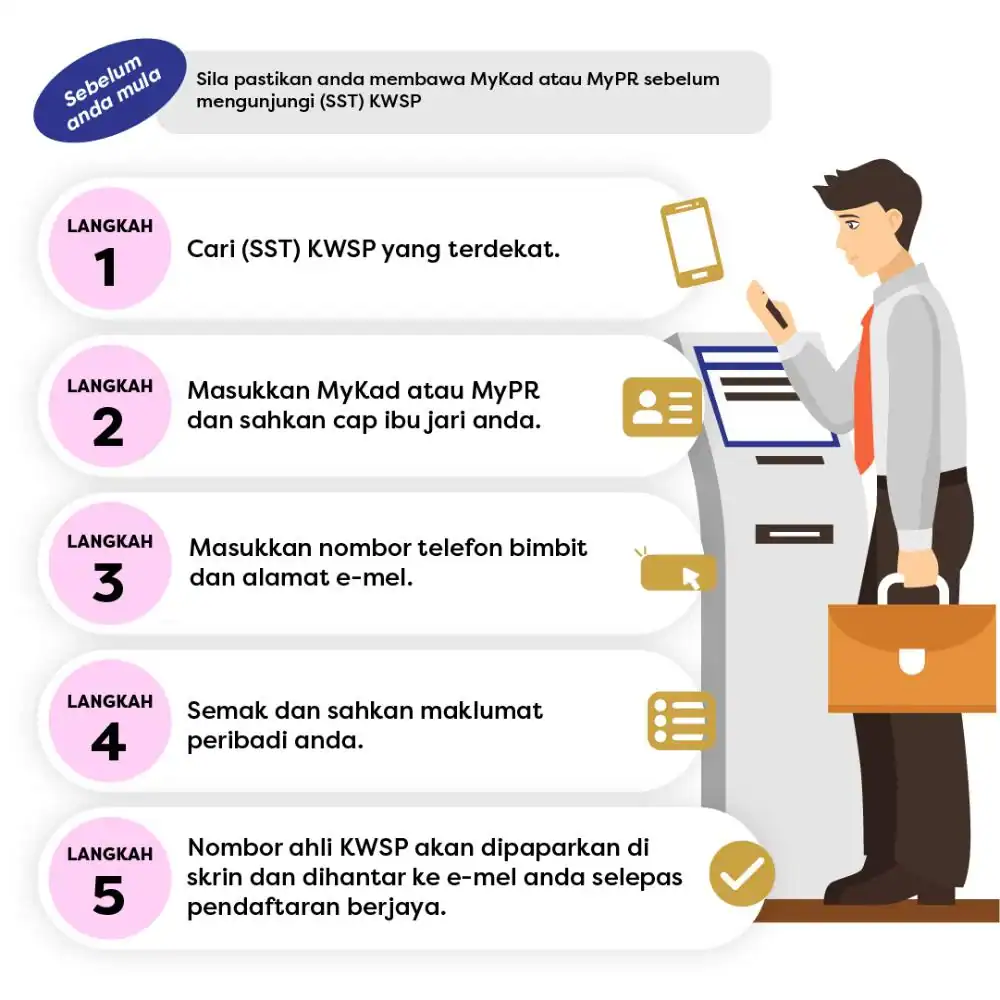

2. Using Self-Service Terminal (SST)

-

Visit a KWSP kiosk

-

Insert MyKad

-

Verify fingerprint

-

Enter your details

3. At KWSP Counter

-

Visit nearest KWSP office

-

Bring MyKad

-

Complete registration

How to Activate i-Saraan

After opening the account:

-

Log in to i-Akaun

-

Select voluntary contribution (i-Saraan)

-

Activate the scheme

-

Start contributing

How to Contribute

You can contribute using:

-

FPX (online banking)

-

JomPAY

-

Auto-debit (recommended)

Auto-debit is helpful because it ensures you save consistently every month without forgetting.

Why Starting Early Matters

Starting early makes a big difference.

If your child starts at 14:

-

They already have savings before working

-

They are ahead compared to others

-

They face less financial pressure later

The same applies to working adults. Starting early and saving consistently is more important than saving a big amount later.

Practical Tips

To make it easier:

-

Set a fixed amount (monthly or yearly)

-

Treat it like a commitment

-

Use auto-debit for consistency

-

Don’t wait for “extra money”

Why This Matters for Work and Future Employees

People who build good saving habits early usually:

-

Manage money better

-

Feel less financial stress

-

Stay more focused at work

For employers, this often means:

-

More stable employees

-

Better productivity

-

Stronger long-term performance

Small financial habits today can shape a better and more stable workforce in the future.

FAQ

What is the minimum age?

14 years old with MyKad.

Can I open it online?

Yes, through i-Akaun with e-KYC.

Who can use i-Saraan?

Parents, freelancers, and working adults.

What is the incentive amount?

20%, up to RM500 per year.

Can money be withdrawn?

Yes, through Account 2 and Account 3.

Want to Build a Better Team?

Financially stable employees tend to be more focused and productive.

Implementing better workforce planning? You may need the right people.

Post your job on AJobThing and reach more candidates faster.

%20copy.jpg)

Read More:

-

Akaun Persaraan KWSP: How It Works & Why It’s Important for Retirement Savings

-

Akaun Sejahtera KWSP: What It Is, How It Works & What You Need to Know

-

EPF SOCSO EIS Contribution 2026: Latest Rates, Rules & Employer Guide in Malaysia

-

How EPF Withdrawal Works When an Employee Leaves Malaysia Permanently

-

Simpanan Shariah KWSP: What It Is, How It Works & What Employers Should Know

-

e-Filing 2026 Malaysia: Opening Date, Deadlines & What Employers Must Know

-

Dividen EPF 2025 (6.15%): Official Rate and What It Means for Employers

-

Pinjaman PTPTN: How to Pay Using KWSP (EPF) Account 2 in 2026

-

Pengeluaran KWSP Untuk Haji 2026: How to Apply & Who Is Eligible

-

EPF i-Lindung Malaysia: Eligibility, Coverage, and How It Works

-

EPF (KWSP) New Updates in January 2026 for Employers & HR in Malaysia

-

Penamaan KWSP in Malaysia: Legal Implications, Process, and HR’s Role

-

Penyata KWSP: How to Check, Download & Understand Your EPF Statement

-

i-Topup KWSP: Contribution Rules & Guide for Employers in Malaysia

-

i-Simpan EPF (KWSP): How It Works & How Employees Can Contribute

-

i-Sayang KWSP Guide: Requirements, Benefits & How to Register

-

EPF, SOCSO, EIS, and LHDN Employer Registration Guide for Malaysian Companies

- Cara Kira Potongan KWSP dan SOCSO | How to Calculate EPF and SOCSO Deductions in Malaysia

-

Deadlines & Penalties for SOCSO, EPF, PCB/Form E, and HRD Levy in Malaysia

-

EPF Withdrawal for Education: Employer’s Guide to Supporting Staff

-

Akaun Fleksibel (EPF’s New Account Structure): Key Info for Employers

-

KWSP Call Centre for Employers: Contact Numbers, Services, and Support Channels