CP22 Form: Deadline, Free Download, & How to Fill

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowHiring a new employee is a milestone for any business, but did you know that failing to report new hires to LHDN could result in fines of up to RM20,000?

Many employers are unaware of the requirement to submit Form CP22 within 30 days of hiring a taxable employee.

Whether you’re new to this process or just need a refresher, this guide covers everything you need to know about CP22, its submission process, and the risks of non-compliance.

What is Form CP22?

The CP22 Form is an official notification that LHDN requires to report new employees liable for income tax.

Employers must submit this form within 30 days of hiring a new employee.

This form helps LHDN track tax obligations by identifying employees who need to pay income tax. It ensures accurate tax records and correct Monthly Tax Deductions (PCB).

Employers must submit CP22 for any new employee earning above the taxable income threshold or those who may become taxable in the future.

If an employee’s salary is initially below the taxable threshold, CP22 is not required.

However, if their income increases to a taxable level later, employers must submit the form as soon as they become taxable.

When Should Employers Submit Form CP22?

Employers are required to submit CP22 within 30 days from the employee’s first working day.

Failing to do so can result in penalties under Section 83(2) of the Income Tax Act 1967, which include:

-

Fines ranging from RM200 to RM20,000

-

Imprisonment of up to six months

-

In some cases, LHDN may hold the employer responsible for the employee’s unpaid taxes

Starting 1 September 2024, all CP22 submissions must be done online via e-CP22 in the MyTax portal. Manual submissions will no longer be accepted.

CP22 vs CP22A

Many employers confuse CP22 and CP22A, but they serve different purposes:

|

Form |

Purpose |

When to Submit? |

|---|---|---|

|

CP22 |

Notifies LHDN about new employees. |

Within 30 days of hiring. |

|

CP22A |

Notifies LHDN when an employee retires, resigns, or permanently leaves Malaysia. |

At least 30 days before the employee’s last working day. |

Both forms must be submitted to LHDN’s nearest branch within the given timeframes.

FREE Download CP22 Form

Download the form for free here.

Step-by-Step Guide to Filling in Form CP22

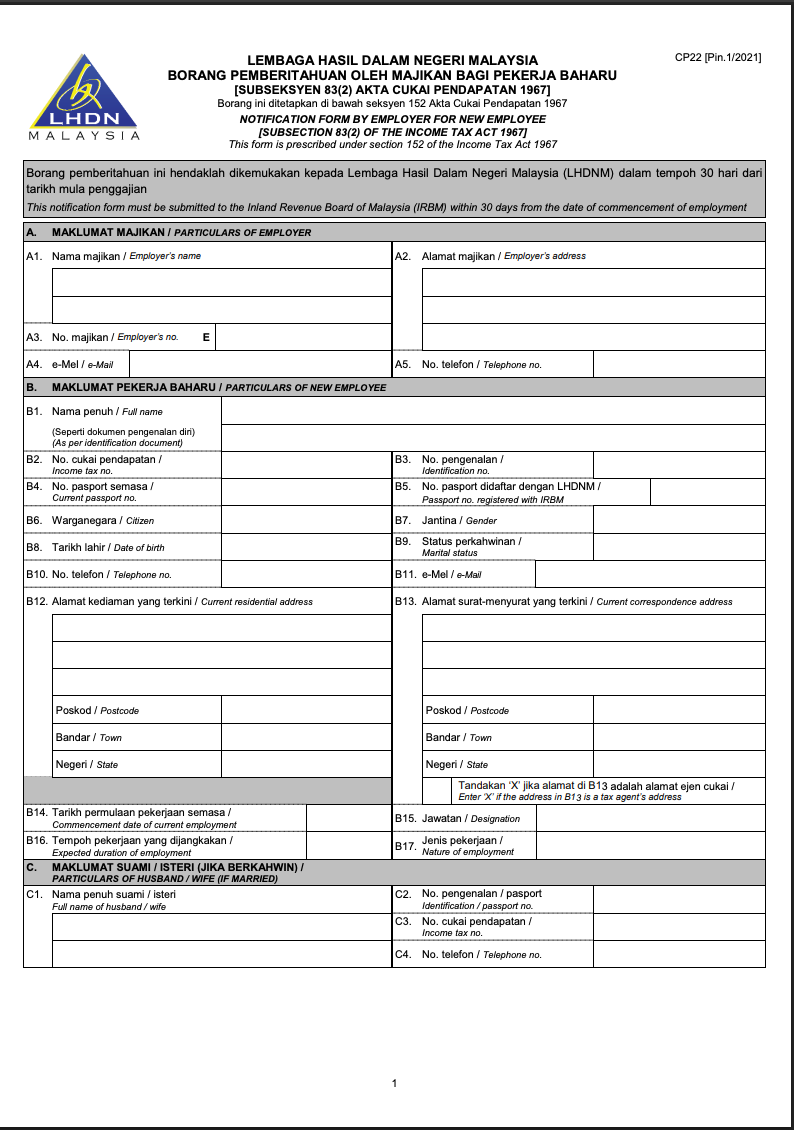

Section A: Employer’s Details

- Employer’s Name – Enter the registered company name.

- Employer’s Tax Reference Number – Provide the company’s income tax file number.

- Employer’s Address – Fill in the full address of the business.

- Employer’s Telephone Number – Provide a valid contact number.

Section B: Employee’s Details

- Employee’s Full Name – As per NRIC or passport.

- Income Tax Number (if available) – If the employee already has an income tax number, enter it.

- New or Existing Employee – Tick the relevant box.

- Identification Details

- NRIC/Passport Number – Malaysian employees use their NRIC number; foreigners use their passport number.

- Nationality – State whether Malaysian or foreign national.

- Date of Birth – As per official documents.

Section C: Employment Information

- Date of Employment – The exact date the employee started working.

- Employee’s Job Title – Specify the position held.

- Monthly Salary & Allowances – Declare the total monthly salary, including bonuses and allowances.

- Employer’s EPF Number – Enter the employee’s EPF (KWSP) number if applicable.

Section D: Other Income Sources (if any)

Indicate whether the employee has other taxable income sources such as rental income or business earnings.

Section E: Declaration

The employer must sign and stamp the form as proof of submission.

Employer Responsibilities After Submitting CP22

Submitting CP22 is just the first step. Employers also have additional responsibilities to stay compliant with tax regulations:

-

Deduct Monthly Tax Deductions (PCB) correctly from the employee’s salary based on their tax bracket to ensure the correct amount is withheld.

-

Keep a copy of CP22 for company records in case of audits or future reference.

-

Document and update all tax-related payroll records regularly to avoid discrepancies and potential compliance issues.

Consequences of Failing to Submit CP22

If businesses do not submit CP22 within 30 days may face some consequences under Section 83(1) of the Income Tax Act 1967 such as:

-

Fines between RM200 and RM20,000 or imprisonment up to six months.

-

LHDN holds the employer responsible for the employee’s unpaid taxes.

-

Reputational damage, such as non-compliance with tax laws can impact business credibility.

FAQ

Is CP22 required for all employees?

No, CP22 is only required for employees who earn above the taxable income threshold or are likely to be taxable.

What if an employee doesn’t have a tax number?

Employers should still submit CP22, and LHDN will assign the employee a Tax Identification Number (TIN) if needed.

Can CP22 be submitted after 30 days?

Yes, but late submission can result in penalties, so it should be done as soon as possible.

What if the employee resigns before CP22 is submitted?

Even if the employee leaves early, CP22 must still be submitted to report their employment history.

What’s the difference between CP22 and CP22A?

CP22 is for new hires, while CP22A is for employees leaving the company due to retirement, resignation, or permanent departure from Malaysia.

While submitting Form CP22 may seem like a minor administrative task, failing to do so can result in serious financial and legal consequences.

Employers who submit CP22 on time help their employees register properly for tax while keeping their businesses free from tax-related complications.

Hiring new employees?

Form CP22 submission is just one step—finding the right talent is the real challenge.

At AJobThing, we connect you with 5+ million jobseekers in Malaysia, ensuring you hire the best while staying compliant with LHDN regulations.

Post your job ads today & simplify your hiring process!

Read More:

- TP1, TP2, and TP3 Forms Malaysia: Definition, Requirements, Free Download Form

- CP204: Deadline, Calculation, & Free Download Form

- How to Use ByrHASiL for Online Tax Payments in Malaysia

- PCB Deduction in Malaysia: Calculation, Rates & Employer Guide

- What is the 182 Days Rule in Malaysia? Tax Residency Explained

- Labour Law Malaysia Salary Payment For Employers

- Best Answers for 'Why Should We Hire You' – A Guide for Employers

- 12 Employment Types You Need to Know: A Guide for Employers

- What is Precarious Employment? Risks, Challenges, and Solution

- New EPF Retirement Savings: Helping Employers Support Financial Well-Being for Employees

- Higher Pensioners in 2024, Government Set to Finalize Pension Rates

- Lack of Diversity in Candidate Pool: Why It Matters and How to Improve It

- Overtime Pay in Malaysia: Legal Requirement and Calculation