KWSP Withdrawal at Age 55 & 60: Rules, Options & HR Guide for Employers in Malaysia

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowWhen employees reach a certain age, their KWSP account and withdrawal options will change.

For HR and employers, this is important not because you manage their withdrawal directly, but because it affects:

-

Payroll handling

-

Employee planning

-

Workforce management

This guide explains what happens at age 55 and 60, and what HR should prepare.

What Happens When an Employee Turns 55?

At age 55, an employee officially enters early retirement stage under KWSP.

Key Change:

All savings from:

Will be combined into Akaun 55.

What This Means

-

Employees can withdraw all or part of their savings anytime

-

Withdrawal is optional (not mandatory)

-

Employees can still continue working

What Happens If Employee Continues Working After 55?

If the employee is still working:

-

KWSP contribution continues as usual

-

New contributions will go into Akaun Emas

- This account is generally accessible starting at age 60

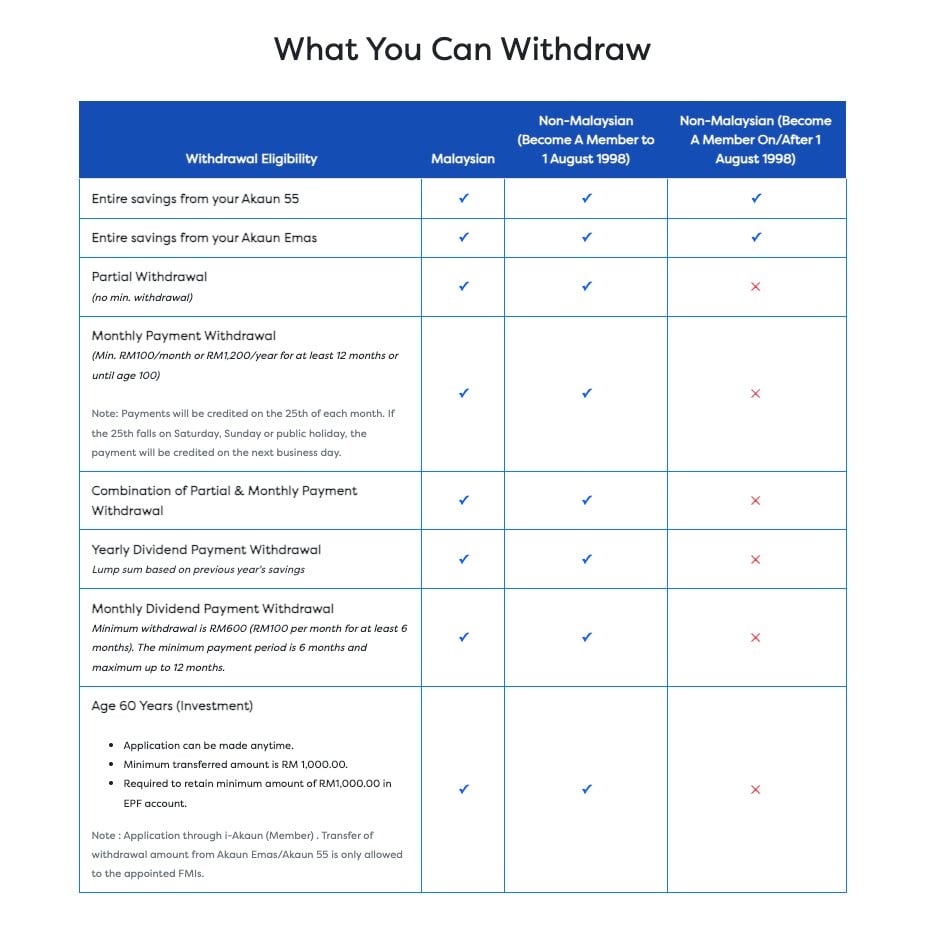

What Happens at Age 60?

At age 60:

-

Employee reaches full retirement age

-

Savings in Akaun Emas can be withdrawn

-

Employee may choose to:

-

Retire fully

-

Continue working

-

Employees will have full access to their retirement savings, including Akaun Emas, subject to KWSP withdrawal rules.

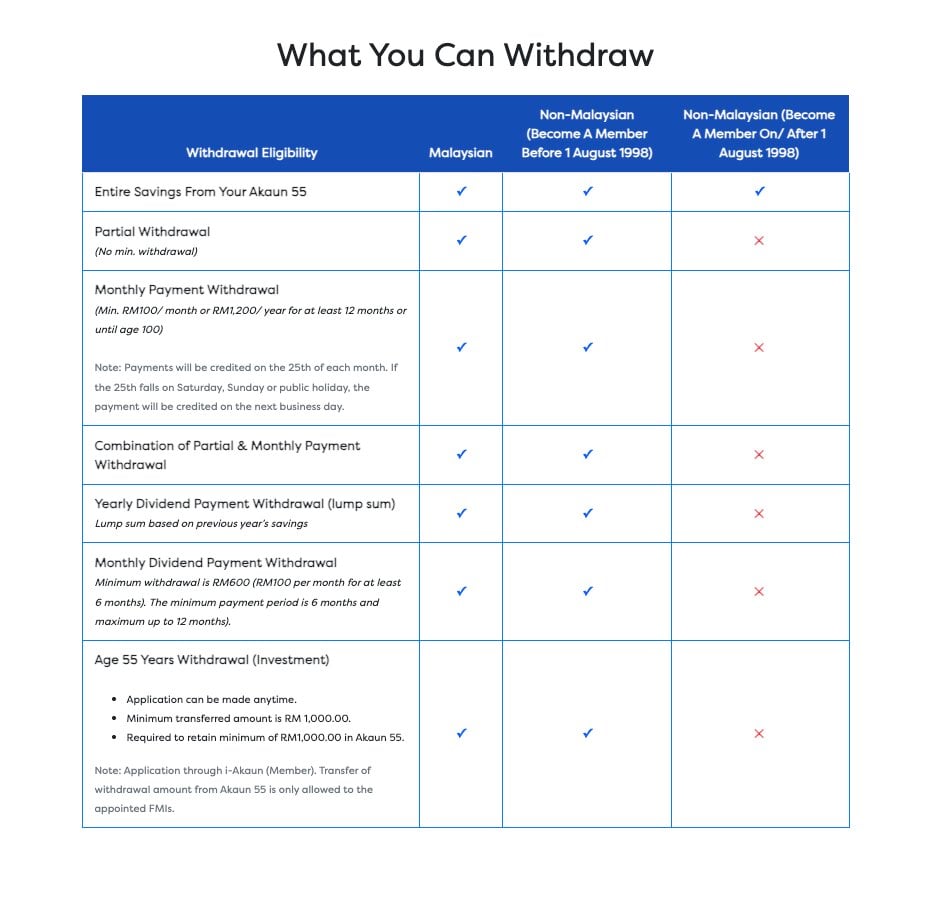

KWSP Withdrawal Options at Age 55

Employees have several options:

-

Full withdrawal (take all savings)

-

Partial withdrawal

-

Monthly withdrawal (minimum RM100/month)

-

Combination of partial + monthly

Image source: Make A Smooth Transition Into Retirement

What HR & Employers Should Pay Attention To

Workforce Planning

Employees aged 55+ may:

-

Consider retirement

-

Request flexible work

-

Reduce working hours

HR should plan early to avoid sudden manpower gaps.

Payroll & Contribution Continuity

As long as employee is still working:

-

KWSP contribution must continue

-

Follow correct rates based on age

Clear Communication

Employees may be confused about:

-

Withdrawal options

-

Contribution after 55

-

Retirement timeline

HR can help by:

-

Sharing simple guidance

-

Avoiding misinformation

Retention Strategy

Senior employees bring:

-

Experience

-

Stability

-

Industry knowledge

Companies may consider:

-

Contract extension

-

Part-time roles

-

Mentorship positions

Special Case: Government Pension Employees

For government employees:

-

They must return government contribution (KWAP)

-

This is handled through Pre-PEN application

HR in government sector must ensure:

-

Proper documentation

-

Correct process before withdrawal

Who Can Apply for Age 55 Withdrawal?

Employees must:

-

Be 55 to 59 years old

-

Have savings in Akaun 55

-

Malaysian or non-Malaysian

Summary

|

Age |

What Happens |

|

55 |

Can withdraw KWSP (optional) |

|

55+ working |

Contributions continue (Akaun Emas) |

|

60 |

Full retirement withdrawal available |

Common Misunderstanding

“Employee withdraw KWSP = must retire”

This is NOT true.

Employees can:

-

Withdraw savings

-

Continue working

Conclusion

KWSP withdrawal at age 55 is mainly for employees, but it still affects employers in terms of planning.

For HR and employers:

-

Understand the change in KWSP structure

-

Continue proper payroll contribution

-

Prepare for employee retirement planning

Managing this well helps ensure:

-

Smooth workforce transition

-

Better employee experience

-

Stronger company planning

FAQ (Quick Answers)

Can employees withdraw KWSP at age 55?

Yes, full or partial withdrawal is allowed

Does employee need to retire at 55?

No, they can continue working

Should employer stop KWSP contribution at 55?

No, contribution continues if employee is still working

What changes at age 60?

Employee can withdraw from Akaun Emas

Does withdrawal affect payroll?

No, unless the employee resigns or retires

Hire & Plan Ahead with AJobThing

%20copy.jpg)

As employees move closer to retirement, workforce planning becomes more important.

With AJobThing, you can:

-

Post job ads quickly

-

Find replacement staff faster

-

Reduce hiring delays

Start posting your job ads today and fill your roles faster before talent moves to competitors.

Read More:

-

Common HR Problems in SMEs Malaysia: Hiring, Payroll & Compliance Solutions

-

e-Filing 2026 Malaysia: Opening Date, Deadlines & Complete Guide

-

EPF Dividends Remain Tax-Free, Says LHDN Amid 2% Dividend Tax Confusion

-

Akaun Persaraan KWSP: How It Works & Why It’s Important for Retirement Savings

-

Akaun Sejahtera KWSP: What It Is, How It Works & What You Need to Know

-

EPF SOCSO EIS Contribution 2026: Latest Rates, Rules & Employer Guide in Malaysia

-

How EPF Withdrawal Works When an Employee Leaves Malaysia Permanently

-

Simpanan Shariah KWSP: What It Is, How It Works & What Employers Should Know

-

e-Filing 2026 Malaysia: Opening Date, Deadlines & What Employers Must Know

-

Pinjaman PTPTN: How to Pay Using KWSP (EPF) Account 2 in 2026

-

Pengeluaran KWSP Untuk Haji 2026: How to Apply & Who Is Eligible

-

EPF i-Lindung Malaysia: Eligibility, Coverage, and How It Works

-

EPF (KWSP) New Updates in January 2026 for Employers & HR in Malaysia

-

Penamaan KWSP in Malaysia: Legal Implications, Process, and HR’s Role

-

Penyata KWSP: How to Check, Download & Understand Your EPF Statement

-

i-Topup KWSP: Contribution Rules & Guide for Employers in Malaysia

-

i-Simpan EPF (KWSP): How It Works & How Employees Can Contribute

-

i-Sayang KWSP Guide: Requirements, Benefits & How to Register

-

EPF, SOCSO, EIS, and LHDN Employer Registration Guide for Malaysian Companies

- Cara Kira Potongan KWSP dan SOCSO | How to Calculate EPF and SOCSO Deductions in Malaysia

-

Deadlines & Penalties for SOCSO, EPF, PCB/Form E, and HRD Levy in Malaysia

-

EPF Withdrawal for Education: Employer’s Guide to Supporting Staff

-

Akaun Fleksibel (EPF’s New Account Structure): Key Info for Employers

-

KWSP Call Centre for Employers: Contact Numbers, Services, and Support Channels