CP204: Deadline, Calculation, & Free Download Form

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowMissing out on tax requirements—especially CP204—can lead to penalties, cash flow problems, and unnecessary stress.

The good news? You're not alone in this. CP204, also known as the Tax Estimate Form, helps businesses stay compliant and manage corporate taxes smoothly.

This guide will break everything down for you—why CP204 matters, deadline, how to submit it, and its calculation.

Let’s make tax filing less of a headache so you can focus on growing your business with confidence!

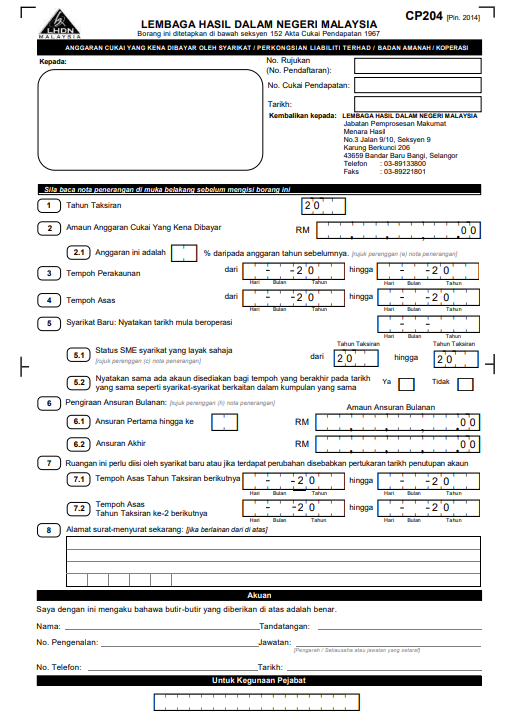

What is CP204?

CP204, also known as the Tax Estimate Form (Borang Anggaran Cukai), is a mandatory tax estimate submission required by the Inland Revenue Board of Malaysia (LHDN) under Section 107C of the Income Tax Act 1967.

This form helps businesses estimate their corporate tax liability for the assessment year and pay it in monthly installments.

The CP204 form applies to businesses with an annual taxable income exceeding RM20,000.

CP204 vs CP204A: What’s the Difference?

Many employers confuse CP204 with CP204A. Here’s the key distinction:

|

Form |

Purpose |

|---|---|

|

CP204 |

The initial tax estimate form that must be submitted by businesses at the beginning of the assessment year. |

|

CP204A |

The revision form used to update the tax estimate if business conditions change during the year. |

Businesses can revise their tax estimate through CP204A in the 6th or 9th month of the financial year, allowing adjustments based on financial performance.

Who Should Submit CP204 Payment?

All companies, Limited Liability Partnerships (LLPs), and cooperative societies with a taxable income exceeding RM20,000 must submit CP204.

Even if your company is newly established, you still need to provide an estimated tax amount if your projected revenue is above the threshold.

When Should Employers Submit CP204?

For Existing Businesses

Companies, LLPs, trusts, and cooperatives that are already operating must submit CP204 at least 30 days before the start of the basis period for the assessment year, as required under subsection 107C(2) of the ITA.

For New Businesses

For newly established companies, LLPs, trusts, and cooperatives with a first basis period of at least six (6) months, CP204 must be submitted within three (3) months from the start of operations, based on paragraph 107C(4)(a) of the ITA.

Special Rule for Second Year Onwards

Starting from the second year of assessment, companies must submit CP204 no later than 30 days before the basis period begins, as stated in paragraph 107C(4)(b) of the ITA.

Example

Mawar Sdn. Bhd. was incorporated on 27 February 2021 and began operations on 3 April 2021. Since its first accounting period ended on 31 December 2021 (9 months), the company had to submit CP204 for Year of Assessment 2021 by 30 June 2021, which is three (3) months after business operations started.

The monthly installment payments began in the 6th month of the basis period, from September 2021 to May 2022.

How to Determine the Amount of Tax Estimate?

The tax estimate should be based on your company’s financial performance.

According to Subsection 107C(3) of the ITA, the estimated tax for a given year must be at least 85% of either the revised tax estimate or the original estimate from the previous year (if no revision was made).

For newly established companies, LLPs, trusts, and cooperatives, the estimated tax for the first year is based on projected profits.

This first-year estimate will then be used as a reference for the following year's tax calculation.

However, the 85% minimum rule under Subsection 107C(3) only applies from the second year onward, as stated in Paragraph 107C(4)(b) of the ITA.

How to Calculate Tax Estimate for CP204?

To calculate the estimated tax for CP204, follow these steps:

-

Determine Taxable Income: Calculate your company’s projected revenue and deduct allowable expenses.

-

Apply Corporate Tax Rate: Malaysia’s corporate tax rates are:

-

17% for the first RM600,000 of chargeable income (for SMEs)

-

24% for chargeable income exceeding RM600,000

-

-

Compare with Previous Year’s Tax: Ensure the estimated tax is at least 85% of the prior year’s tax liability.

-

Divide into Monthly Installments: The estimated tax must be paid in 12 equal monthly installments.

Example: If your estimated chargeable income is RM1,000,000:

|

Chargeable Income |

Tax Rate |

Tax Amount |

|---|---|---|

|

RM600,000 |

17% |

RM102,000 |

|

RM400,000 |

24% |

RM96,000 |

|

Total Tax Payable |

RM198,000 |

|

|

Monthly Installment |

RM16,500 (RM198,000/12 months) |

How to Do Revision for CP204?

Businesses such as companies, LLPs, trusts, and cooperatives can update their estimated tax payments by submitting Form CP204A through the e-CP204A system.

This is allowed under subsection 107C(7) of the Income Tax Act (ITA).

When Can You Amend CP204?

You can revise Form CP204 in the 6th, 9th, or 11th month of the assessment year. Changes made will affect future tax installment payments as shown in the table below:

|

Amendment Month |

New Installment Starts From |

|---|---|

|

6th month |

5th or 6th installment |

|

9th month |

8th or 9th installment |

|

11th month |

11th installment |

This flexibility allows businesses to adjust their tax estimates based on updated financial performance.

How is the Instalment Amount Determined?

The amount you need to pay in tax installments can change depending on whether your estimated tax increases or decreases. Below are two scenarios explaining how your revised installment amount is determined.

Scenario 1: If the Revised Estimated Tax is Higher

If your new estimated tax amount is higher than the original amount, your remaining installments will be adjusted. The balance must be paid in equal monthly installments over the remaining months.

Example:

-

Assessment Year: 2023

-

Tax Period: 01.01.2023 – 31.12.2023

-

Initial Estimated Tax: RM120,000 (RM10,000 per month)

-

Revised Estimated Tax (from the 6th month): RM260,000

New Monthly Installment Calculation:

New Payment Schedule:

|

Installment No. |

Due Date |

Original Amount (RM) |

Revised Amount (RM) |

|---|---|---|---|

|

1 |

15.02.2023 |

10,000.00 |

10,000.00 |

|

2 |

15.03.2023 |

10,000.00 |

10,000.00 |

|

3 |

15.04.2023 |

10,000.00 |

10,000.00 |

|

4 |

15.05.2023 |

10,000.00 |

10,000.00 |

|

5 |

15.06.2023 |

10,000.00 |

10,000.00 |

|

6 |

15.07.2023 |

10,000.00 |

30,000.00 |

|

7 |

15.08.2023 |

10,000.00 |

30,000.00 |

|

8 |

15.09.2023 |

10,000.00 |

30,000.00 |

|

9 |

15.10.2023 |

10,000.00 |

30,000.00 |

|

10 |

15.11.2023 |

10,000.00 |

30,000.00 |

|

11 |

15.12.2023 |

10,000.00 |

30,000.00 |

|

12 |

15.01.2024 |

10,000.00 |

30,000.00 |

|

Total |

- |

120,000.00 |

260,000.00 |

Scenario 2: If the Revised Estimated Tax is Lower

If your new estimated tax is lower than the original amount, future payments may stop once the total amount reaches the new estimate.

Example:

-

Tax Period: 01.04.2023 – 31.03.2024

-

Initial Estimated Tax: RM360,000 (RM30,000 per month)

-

Revised Estimated Tax (from the 8th month): RM200,000

New Monthly Installment Calculation:

New Payment Schedule:

|

Installment No. |

Due Date |

Original Amount (RM) |

Revised Amount (RM) |

|---|---|---|---|

|

1 |

15.05.2023 |

30,000.00 |

30,000.00 |

|

2 |

15.06.2023 |

30,000.00 |

30,000.00 |

|

3 |

15.07.2023 |

30,000.00 |

30,000.00 |

|

4 |

15.08.2023 |

30,000.00 |

30,000.00 |

|

5 |

15.09.2023 |

30,000.00 |

30,000.00 |

|

6 |

15.10.2023 |

30,000.00 |

30,000.00 |

|

7 |

15.11.2023 |

30,000.00 |

30,000.00 |

|

8 |

15.12.2023 |

30,000.00 |

0.00 |

|

9 |

15.01.2024 |

30,000.00 |

0.00 |

|

10 |

15.02.2024 |

30,000.00 |

0.00 |

|

11 |

15.03.2024 |

30,000.00 |

0.00 |

|

12 |

15.04.2024 |

30,000.00 |

0.00 |

|

Total |

- |

360,000.00 |

210,000.00 |

This method ensures that your tax installments remain fair and accurate based on your updated estimated tax liability.

Payment Schedule for Estimated Tax

For businesses like companies, LLPs, trusts, and cooperatives that are already operating, the estimated tax must be paid in equal monthly installments.

These payments start from the second month of the tax year and must be made by the due date each month.

For newly established businesses, tax payments also follow a monthly installment plan, but payments start from the sixth month of the tax year.

The due date for each installment is the 15th of every month.

|

Start Date of Basis Period |

Submission Deadline |

First Installment Payment Month |

|---|---|---|

|

01/01/2023 |

01/12/2022 |

Feb 2023 |

|

01/02/2023 |

01/01/2023 |

Mar 2023 |

|

01/03/2023 |

29/01/2023 |

Apr 2023 |

|

01/04/2023 |

01/03/2023 |

May 2023 |

|

01/05/2023 |

31/03/2023 |

June 2023 |

|

01/06/2023 |

01/05/2023 |

Jul 2023 |

|

01/07/2023 |

31/05/2023 |

Aug 2023 |

|

01/08/2023 |

01/07/2023 |

Sept 2023 |

|

01/09/2023 |

01/08/2023 |

Oct 2023 |

|

01/10/2023 |

31/08/2023 |

Nov 2023 |

|

01/11/2023 |

01/10/2023 |

Dec 2023 |

|

01/12/2023 |

31/10/2023 |

Jan 2024 |

Example: Estimated Tax Installment Calculation

For a company in operation in 2023:

-

Estimated tax amount: RM130,000

-

Basis period: 01/01/2023 – 31/12/2023

-

Number of installments: 12

-

First installment: Starts on February 15, ends on January 15 of the following year

Monthly Installments Calculation

|

Installment Number |

Amount (RM) |

|---|---|

|

1-11 |

10,833 |

|

12 |

10,837 |

Note: If the estimated tax is not evenly divisible by the number of months, the remaining balance is added to the final installment.

Penalties for Late Submission, Non-Payment, or Incorrect Tax Estimate in CP204

If a company, LLP, trust, or cooperative does not submit Form CP204, the following actions may be taken:

|

Consequence |

Details |

|---|---|

|

Estimated Tax Assessment |

The Inland Revenue Board (IRB) will estimate the tax payable and issue a Notice of Instalment Payment (CP205) under subsection 107C(8) of the Income Tax Act (ITA). |

|

Legal Penalty |

The company may face legal action under paragraph 120(1)(f) of the ITA. |

|

Fines & Imprisonment |

If convicted, the penalty may include a fine between RM200 and RM20,000, imprisonment for up to 6 months, or both. |

To avoid these penalties, businesses should ensure timely submission of Form CP204.

How to Pay CP204?

Employers can pay CP204 through various methods, including:

|

Payment Method |

Description |

|---|---|

|

Cheque or Bank Draft |

Payable to LHDN offices. |

|

Online Banking |

FPX, CIMB Clicks, Maybank2U, and other banks. |

|

LHDN Payment Kiosks |

Available for over-the-counter payments. |

|

Auto-Debit |

Direct deduction from company bank accounts. |

Download Form & How to Fill

You can download the CP204 and CP204A forms from the official LHDN website:

To fill out CP204:

-

Enter company details and tax reference number.

-

Provide the estimated tax amount.

-

Indicate the tax installment amount.

-

Submit the completed form to LHDN via e-Filing or at an LHDN branch.

Submitting CP204 correctly is crucial for Malaysian businesses to comply with tax regulations and avoid penalties. By estimating and revising tax estimates accurately, employers can manage cash flow efficiently.

Need to hire new employees? We have 5+ Millions Talents in Malaysia

Start your hiring journey with AJobThing today! Post your job ads, connect with top talents, and streamline your recruitment process with our easy-to-use platform.

Read More:

- How to Use ByrHASiL for Online Tax Payments in Malaysia

- PCB Deduction in Malaysia: Calculation, Rates & Employer Guide

- What is the 182 Days Rule in Malaysia? Tax Residency Explained

- Labour Law Malaysia Salary Payment For Employers

- Best Answers for 'Why Should We Hire You' – A Guide for Employers

- 12 Employment Types You Need to Know: A Guide for Employers

- What is Precarious Employment? Risks, Challenges, and Solution

- New EPF Retirement Savings: Helping Employers Support Financial Well-Being for Employees

- Higher Pensioners in 2024, Government Set to Finalize Pension Rates

- Lack of Diversity in Candidate Pool: Why It Matters and How to Improve It

- Overtime Pay in Malaysia: Legal Requirement and Calculation