EPF Akaun Fleksibel: How Your Dividends Are Calculated

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowFollowing the latest EPF dividend announcement, many Malaysians have been asking:

-

How are dividends for Akaun Fleksibel calculated?

-

Does withdrawing money reduce my dividend?

-

Why is my dividend different from someone else's, even though we earn similar salaries?

Understanding how Akaun Fleksibel dividends work can help employees make better financial decisions and enable employers and HR teams to answer common employee questions more effectively.

What Is Akaun Fleksibel?

Akaun Fleksibel was introduced on 11 May 2024 as part of EPF's account restructuring to provide members with greater flexibility in accessing their retirement savings.

Today, monthly EPF contributions are allocated as follows:

|

EPF Account |

Allocation |

|

Akaun Persaraan |

75% |

|

15% |

|

|

10% |

Unlike the other two accounts, Akaun Fleksibel allows members to withdraw their savings at any time, subject to EPF's terms and conditions.

Example

If an employee earns RM4,000 per month and the total EPF contribution is RM960, the allocation would be:

|

Account |

Amount |

|

Akaun Persaraan |

RM720 |

|

Akaun Sejahtera |

RM144 |

|

Akaun Fleksibel |

RM96 |

This means RM96 is credited into Akaun Fleksibel every month.

How Are Akaun Fleksibel Dividends Calculated?

EPF calculates dividends using the Modified Aggregate Daily Balance (MADB) method.

Simply put, your dividend depends on:

-

How much money is in your account.

-

How long the money stays in your account.

-

Whether you make any withdrawals during the year.

The longer your money remains in Akaun Fleksibel, the more dividends it can potentially earn.

Dividend Formula

Dividend = Daily Balance × Dividend Rate × Number of Days ÷ 365

For illustration purposes only, let's assume the EPF dividend rate is 6.30%

Important Rule #1: New Contributions Do Not Earn Dividends Immediately

Contributions received during a particular month only start generating dividends on the last day of that month.

Example

If RM100 is contributed on 1 January, it only earns dividends for one day in January (31 January). The full daily dividend calculation begins from 1 February onwards.

Important Rule #2: Withdrawals Stop Earning Dividends Immediately

Once money is withdrawn from Akaun Fleksibel, that amount immediately stops generating dividends.

This means the timing of withdrawals can significantly affect your annual dividend earnings.

Example: Calculating Your Annual Dividend

Suppose an employee keeps RM5,000 in Akaun Fleksibel for the entire year without making any withdrawals.

Calculation:

RM5,000 × 6.30% × 365 ÷ 365 = RM315

|

Opening Balance |

Annual Dividend |

Year-End Balance |

|

RM5,000 |

RM315 |

RM5,315 |

By simply leaving the money untouched, the employee earns RM315 in dividends for the year.

Example: How a Withdrawal Can Reduce Your Dividend

Now suppose the employee withdraws RM4,000 from Akaun Fleksibel on 1 February.

The remaining balance becomes RM1,000.

Calculation:

RM1,000 × 6.30% × 365 ÷ 365 = RM63

|

Scenario |

Annual Dividend |

|

No withdrawal |

RM315 |

|

Withdraw RM4,000 |

RM63 |

Difference

RM252 less in dividends for the year.

This example shows why frequent withdrawals can significantly reduce long-term savings growth.

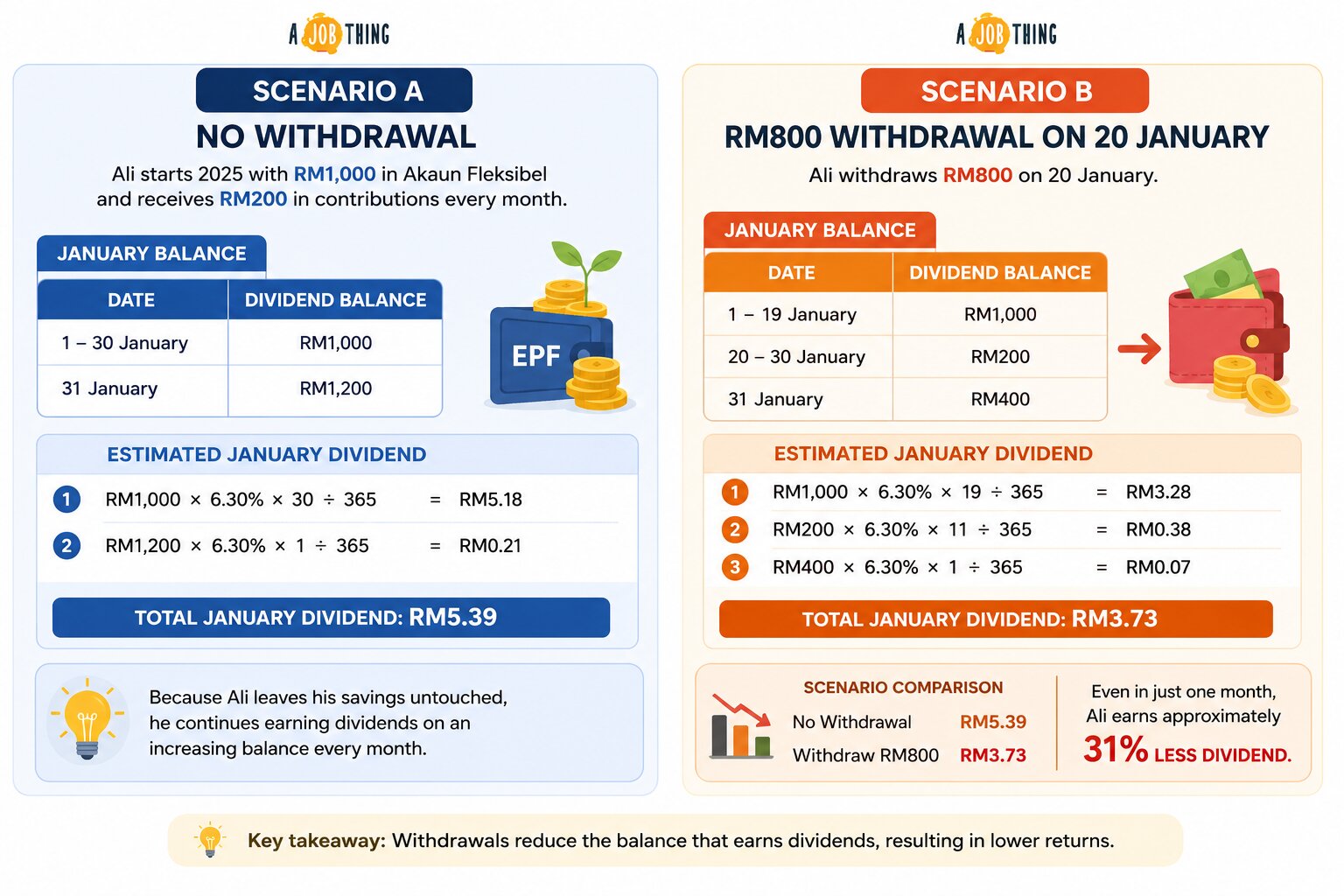

Scenario A: No Withdrawal

Ali starts 2025 with RM1,000 in Akaun Fleksibel and receives RM200 in contributions every month.

January Balance

|

Date |

Dividend Balance |

|

1–30 January |

RM1,000 |

|

31 January |

RM1,200 |

Estimated January dividend:

-

RM1,000 × 6.30% × 30 ÷ 365 = RM5.18

-

RM1,200 × 6.30% × 1 ÷ 365 = RM0.21

Total January dividend: RM5.39

Because Ali leaves his savings untouched, he continues earning dividends on an increasing balance every month.

Scenario B: RM800 Withdrawal on 20 January

Ali withdraws RM800 on 20 January.

January Balance

|

Date |

Dividend Balance |

|

1–19 January |

RM1,000 |

|

20–30 January |

RM200 |

|

31 January |

RM400 |

Estimated January dividend:

-

RM1,000 × 6.30% × 19 ÷ 365 = RM3.28

-

RM200 × 6.30% × 11 ÷ 365 = RM0.38

-

RM400 × 6.30% × 1 ÷ 365 = RM0.07

Total January dividend: RM3.73

|

Scenario |

January Dividend |

|

No Withdrawal |

RM5.39 |

|

Withdraw RM800 |

RM3.73 |

Even in just one month, Ali earns approximately 31% less dividend.

Want to estimate your monthly EPF contributions and deductions? Use this free EPF Calculator to better understand your savings and retirement planning.

Why This Matters for Employees

Before making a withdrawal, employees should ask themselves:

-

Is this an emergency expense?

-

Do I have other savings available?

-

Am I comfortable receiving lower dividends this year?

-

Will this withdrawal affect my long-term retirement savings?

Every withdrawal reduces not only the current year's dividend but also the amount available to continue compounding over time.

Why This Matters for Employers and HR

Many HR teams receive questions such as:

-

Why is my EPF dividend lower this year?

-

Did my withdrawal affect my dividend?

-

Why didn't my latest contribution earn dividends immediately?

-

Why did my colleague receive a higher dividend even though we have similar salaries?

Understanding how Akaun Fleksibel works allows employers to better support employee financial wellbeing.

Financially Informed Employees are More Likely To:

-

Experience less financial stress.

-

Make better long-term financial decisions.

-

Appreciate their employment benefits.

-

Be more engaged and productive at work.

Employers can also include EPF education as part of their financial wellness programmes to improve employee wellbeing and retention.

Tips to Maximise Your Akaun Fleksibel Dividend

-

Keep your savings in the account for as long as possible.

-

Avoid unnecessary withdrawals.

-

Remember that every ringgit left in the account continues generating dividends.

-

Use Akaun Fleksibel primarily for emergencies or essential expenses.

-

Allow your savings to benefit from the compounding effect of annual dividends.

FAQs

Does withdrawing from Akaun Fleksibel reduce my dividend?

Yes. The withdrawn amount immediately stops generating dividends from the withdrawal date.

Which EPF account receives the highest dividend?

All three EPF accounts receive the same annual dividend rate.

Can I return money that I withdrew back into Akaun Fleksibel?

No. EPF contributions follow the official allocation formula and cannot be manually reallocated.

Will I still receive dividends if my balance becomes RM0?

Yes. You will still receive dividends earned before your balance became RM0. However, once the balance reaches RM0 and no new contributions are made, the account will stop generating dividends.

Is Akaun Fleksibel suitable for emergency savings?

Akaun Fleksibel can provide short-term financial relief during emergencies. However, frequent withdrawals may significantly reduce long-term retirement savings and dividend earnings.

Your Next Hire Could be Just a Click Away!

%20copy.jpg)

At AJobThing, we connect you with million jobseekers in Malaysia, ensuring you hire the best.

Post your job ads today & simplify your hiring process!

Read More:

-

How to Reset Your i-Akaun (Member) Password Via The KWSP i-Akaun App

-

EPF (KWSP) Contribution Rates 2026: How Much Do Employees and Employers Contribute?

-

PERKESO Lindung 24 Jam: How Much Will Be Deducted From Your Salary?

-

SOCSO "Lindung 24 Jam": New Employee Contribution Scheme Effective 1 June 2026

-

9 Types of Skim KWSP in 2026: Which One Fits Your Retirement Goals?

-

EIS PERKESO Login: How to Claim SIP & Elaun Kehilangan Pekerjaan

-

KWSP untuk Ansuran Rumah (2026): How It Works & Who Can Apply

-

EPF Account Restructuring Guide: Akaun Fleksibel, Sejahtera & Persaraan

-

How to Calculate EPF (KWSP) in Malaysia: Contribution Rates, Payment & Rules

-

EPF Employer Responsibilities in Malaysia: Rules, Contributions & Compliance Guide

-

EPF Death Assistance Malaysia: Eligibility, Claims Process & HR Guide

-

EPF, SOCSO & EIS Contribution for Part-Time, Contract & Foreign Workers in Malaysia

-

KWSP Akaun Emas Rules and Withdrawal After Age 55 in Malaysia

-

i-Saraan Plus: Employer Guide to EPF Incentives for E-Hailing & P-Hailing Drivers in Malaysia

-

i-Suri KWSP 2026 Malaysia: Benefits, Eligibility & How It Works

-

e-Filing 2026 Malaysia: Opening Date, Deadlines & Complete Guide

-

EPF Dividends Remain Tax-Free, Says LHDN Amid 2% Dividend Tax Confusion

-

Akaun Persaraan KWSP: How It Works & Why It’s Important for Retirement Savings

-

Akaun Sejahtera KWSP: What It Is, How It Works & What You Need to Know

-

EPF SOCSO EIS Contribution 2026: Latest Rates, Rules & Employer Guide in Malaysia

-

How EPF Withdrawal Works When an Employee Leaves Malaysia Permanently

-

Simpanan Shariah KWSP: What It Is, How It Works & What Employers Should Know

-

e-Filing 2026 Malaysia: Opening Date, Deadlines & What Employers Must Know

-

Pinjaman PTPTN: How to Pay Using KWSP (EPF) Account 2 in 2026

-

Pengeluaran KWSP Untuk Haji 2026: How to Apply & Who Is Eligible

-

EPF i-Lindung Malaysia: Eligibility, Coverage, and How It Works

-

EPF (KWSP) New Updates in January 2026 for Employers & HR in Malaysia

-

Penamaan KWSP in Malaysia: Legal Implications, Process, and HR’s Role

-

Penyata KWSP: How to Check, Download & Understand Your EPF Statement

-

i-Topup KWSP: Contribution Rules & Guide for Employers in Malaysia

-

i-Simpan EPF (KWSP): How It Works & How Employees Can Contribute

-

i-Sayang KWSP Guide: Requirements, Benefits & How to Register

-

EPF, SOCSO, EIS, and LHDN Employer Registration Guide for Malaysian Companies

- Cara Kira Potongan KWSP dan SOCSO | How to Calculate EPF and SOCSO Deductions in Malaysia

-

Deadlines & Penalties for SOCSO, EPF, PCB/Form E, and HRD Levy in Malaysia

-

EPF Withdrawal for Education: Employer’s Guide to Supporting Staff

-

Akaun Fleksibel (EPF’s New Account Structure): Key Info for Employers

-

KWSP Call Centre for Employers: Contact Numbers, Services, and Support Channels