EPF i-Lindung Malaysia: Eligibility, Coverage, and How It Works

Are You Hiring?

Find candidates in 72 Hours with 5+ million talents in Maukerja Malaysia & Ricebowl using Job Ads.

Hire NowAs healthcare costs rise and personal financial risks become more complex, employee protection has become a growing concern in Malaysia. While many employers provide group medical or insurance benefits, not all employees are fully covered, especially lower-income earners, contract staff, or those without company insurance plans.

To help address this protection gap, the Employees Provident Fund (EPF), also known as KWSP, introduced EPF i-Lindung.It allows members to purchase insurance or takaful coverage using part of their EPF savings.

What Is EPF i-Lindung?

EPF i-Lindung is an official initiative by KWSP (Employees Provident Fund) that enables EPF members to purchase selected insurance or takaful products through the KWSP i-Akaun platform. It is:

-

A self-service online platform

-

Offered under the Members Protection Plan (MPP)

-

Provided by insurance and takaful operators (ITOs) approved by EPF

-

Voluntary and optional for members

Payments for i-Lindung products are made using the member’s EPF savings, subject to eligibility and available balance.

Why EPF Introduced i-Lindung

EPF introduced i-Lindung to improve financial protection for Malaysians, especially those without sufficient personal insurance coverage.

Key reasons include:

-

A growing protection gap among working Malaysians

-

Rising medical costs and income-loss risks

-

Limited access to affordable insurance for some workers

-

The need to strengthen long-term financial resilience

i-Lindung is intended to complement and not replace the existing insurance arrangements.

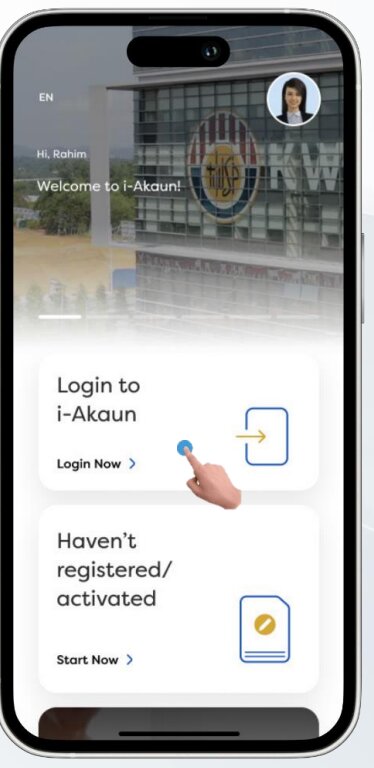

How EPF i-Lindung Works

The process is designed to be simple and fully online:

-

Member logs in to KWSP i-Akaun (Member)

-

Navigates to the “i-Lindung” section

-

Selects from available insurance or takaful products offered by approved ITOs

-

Payment is made using eligible EPF savings

-

Coverage begins after approval by the insurance or takaful provider

Important points to note:

-

No cash payment is required

-

No salary deduction is involved

-

EPF savings are used directly

-

EPF does not act as the insurer or takaful operator

Who Is Eligible for EPF i-Lindung

Eligibility is subject to EPF rules and insurer requirements. Generally, applicants must be:

-

Active EPF members

-

Malaysian citizens

-

Have a sufficient balance in the relevant EPF account

-

Meet the underwriting criteria set by the insurance or takaful provider

Members with disabilities (OKU) or their representatives may liaise directly with the relevant ITO to explore suitable products.

Who Can Be Covered Under i-Lindung?

Coverage may include:

-

The EPF member (primary protected person)

-

Spouse (dependent)

-

Children (dependents)

Children include biological children, stepchildren, and legally adopted children. The number of dependents covered is subject to product limits set by the ITO.

Types of Protection Available Under i-Lindung

Coverage options vary by provider, but may include:

-

Income protection (depending on the provider)

-

Life insurance or family takaful

-

Critical illness protection

-

Other protection products approved under the MPP

Not all products are identical, and availability depends on the participating insurer or takaful operator.

Key Benefits of EPF i-Lindung for Employees

EPF i-Lindung offers employees an alternative way to access insurance or takaful protection, especially for those who may not have sufficient personal coverage.

Key benefits include:

Access to Protection without Monthly Cash Payments

Employees can use part of their EPF savings to pay for insurance or takaful premiums, reducing the need for immediate out-of-pocket expenses.

Easier Access for Lower-Income Earners

For employees who may find regular premium payments challenging, i-Lindung provides an option to obtain protection using existing EPF balances, subject to eligibility.

Centralised Platform Under EPF

All applications are made through KWSP i-Akaun, allowing members to view available products in one place rather than approaching multiple providers separately.

Choice Between Insurance and Takaful Products

Employees can select products that suit their personal, financial, or religious preferences, including Shariah-compliant takaful options.

Supports Personal Financial Resilience

While i-Lindung does not replace retirement planning, it helps employees manage financial risks such as illness or loss of income that could otherwise impact long-term savings.

Why EPF i-Lindung Matters for Employers & HR Teams

While employers do not manage or fund i-Lindung, understanding it helps HR teams support employees more effectively. i-Lindung can:

-

Complement company medical or insurance benefits

-

Support employees without group insurance coverage

-

Reduce financial stress among staff

-

Strengthen employee wellbeing initiatives

-

Enhance financial literacy programmes

Employers often share i-Lindung information during onboarding, HR briefings, or employee education sessions.

How Employers Commonly Use EPF i-Lindung Information

Although employers are not involved in managing or funding EPF i-Lindung, many HR teams find it helpful to understand the platform so they can guide employees accurately.

Common use cases include:

Employee Onboarding and Orientation

HR teams may briefly introduce i-Lindung as part of EPF-related education, especially for new hires unfamiliar with EPF options beyond contributions.

HR Briefings and Internal Communications

During town halls or HR updates, employers may share general information about i-Lindung to help employees understand available personal protection options.

Supporting Employees without Group Insurance

For companies that do not offer medical or insurance benefits, i-Lindung information can help employees explore individual protection alternatives independently.

Answering EPF-Related Employee Questions

HR teams often receive questions about EPF withdrawals, insurance, or savings usage. Understanding i-Lindung helps HR respond accurately without giving financial advice.

Financial Literacy and Wellbeing Initiatives

Some employers include i-Lindung as part of broader financial education programmes, alongside topics such as EPF savings, retirement planning, and personal insurance awareness.

Important Things to Know About EPF i-Lindung

Before employees decide to participate in EPF i-Lindung, employees need to understand how the platform works and what it does and does not do.

Participation is Fully Voluntary

EPF i-Lindung is optional. Members are not required to join, and there is no obligation to purchase any insurance or takaful product through the platform.

Employers are Not Involved in Payment or Administration

Employers do not pay for i-Lindung premiums, do not manage enrolment, and do not deduct salaries for this purpose. All decisions and applications are made directly by the EPF member.

No Automatic Deductions from EPF Accounts

EPF will not deduct funds automatically. Members must actively select a product and approve the use of their EPF savings through i-Akaun.

Company Insurance Benefits Remain Unchanged

Joining i-Lindung does not replace or affect any existing company-provided medical or insurance benefits. Group insurance coverage continues to apply according to company policy.

EPF Contribution Rates are Not Affected

Using i-Lindung does not change statutory EPF contribution rates made by employers or employees.

Insurance Products are Provided by Approved Insurers and Takaful Operators

EPF provides the platform, but it does not underwrite, manage, or guarantee the insurance or takaful policies offered. Coverage terms depend on the selected provider.

Key Points Employees Should Be Aware Of

Employees considering EPF i-Lindung should review the following carefully before making a decision.

Using EPF Savings May Reduce Retirement Funds

Premium payments are made using EPF savings from Akaun Sejahtera. This means the amount available for long-term retirement may be reduced.

Coverage Terms Differ by Provider and Product

Each insurance or takaful product has its own benefits, exclusions, coverage limits, age requirements, and eligibility criteria. Products are not standardised across providers.

EPF Does Not Handle Claims or Policy Servicing

All claims, policy changes, renewals, and enquiries must be handled directly with the appointed insurance company or takaful operator, not EPF.

Approval is Subject to Insurer requirements

Some products may still involve underwriting conditions or eligibility checks, depending on the insurer and type of coverage selected.

Policy Documents Should be Reviewed Carefully

Employees are advised to read the product disclosure sheet, policy terms, and conditions in full before approving any purchase through i-Lindung.

Takaful Options are Available for Muslim Members

Muslim members are encouraged to choose takaful products, which are Shariah-compliant, instead of conventional insurance.

How to Access EPF i-Lindung

-

Log in to KWSP i-Akaun

-

Select the “i-Lindung” section

-

Review available products

-

Apply directly through the platform

Source: https://www.kwsp.gov.my/documents/d/guest/panduan-mudah-i-lindung_bm

Applications must be made online. Insurance agents are not involved in the purchase process.

Helping Employees Plan Their EPF Savings?

.jpg)

Use our EPF Calculator to estimate contributions accurately and avoid exceeding annual limits.

FAQs

What is EPF i-Lindung?

It is a KWSP platform that allows EPF members to purchase insurance or takaful using EPF savings.

Can employers register employees for i-Lindung?

No. Applications must be made by the EPF member.

Is i-Lindung mandatory?

No. Participation is voluntary.

Can EPF money be used to pay insurance premiums?

Yes, subject to eligibility and available balance.

Does i-Lindung replace company medical insurance?

No. It is meant to complement existing coverage, not replace it.

Your Next Hire Could be Just a Click Away!

At AJobThing, we connect you with 5+ million jobseekers in Malaysia, ensuring you hire the best.

Post your job ads today & simplify your hiring process!

Read More:

-

Zakat Pendapatan in Malaysia: Who Must Pay, How to Calculate, and How to Claim 100% Tax Rebate

-

Skim Jaminan Kredit Perumahan (SJKP): How Malaysians Can Buy a Home Without a Payslip

-

Semakan SARA 2026: Recipient Categories, Payment Dates and How to Use MyKad

-

SARA 2026 Malaysia: Eligibility, Payment Dates, Amount & MyKad Usage

-

i-Topup KWSP: Contribution Rules & Guide for Employers in Malaysia

-

i-Simpan EPF (KWSP): How It Works & How Employees Can Contribute

-

EPF (KWSP) New Updates in January 2026 for Employers & HR in Malaysia

-

Penamaan KWSP in Malaysia: Legal Implications, Process, and HR’s Role

-

i-Sayang KWSP Guide: Requirements, Benefits & How to Register

-

EPF, SOCSO, EIS, and LHDN Employer Registration Guide for Malaysian Companies

- Cara Kira Potongan KWSP dan SOCSO | How to Calculate EPF and SOCSO Deductions in Malaysia

-

Deadlines & Penalties for SOCSO, EPF, PCB/Form E, and HRD Levy in Malaysia

-

EPF Withdrawal for Education: Employer’s Guide to Supporting Staff

-

Akaun Fleksibel (EPF’s New Account Structure): Key Info for Employers

-

KWSP Call Centre for Employers: Contact Numbers, Services, and Support Channels